What did Simon Flowers say?

Oil and gas investment strategy started getting trickier after the Paris Agreement almost a decade ago. In recent years, the uncertain pace of the energy transition has added another layer of complexity, making annual planning decisions a bit like three-dimensional chess. How much capital to allocate to oil and gas versus building a sustainable business in low carbon for the longer term – all the while meeting the financial expectations of stakeholders? This year, the implications for oil and gas markets of the grave escalation of conflict in the Middle East compound the challenge.

Our Corporate Strategic Planner is a new addition from our Corporate Strategy and Analytics Service. It’s designed to help oil and gas companies, advisors and shareholders anticipate and navigate the key themes in their annual planning and capital allocation cycle.

I asked Tom Ellacott, Neivan Boroujerdi, Alex Beeker and Rapha Portela from our Corporate Analysis team how they see 2025 shaping up for the 32 companies they’ve analysed spread across US Majors, EuroMajors, Emerging Majors and NOCs.

Are companies planning to spend more in 2025?

Yes, we’re about to enter the fifth year of an upcycle. By the end of this year, annual investment for these 32 companies will have risen more than 60% from the 2020 low during the pandemic. But we expect growth to slow to about 5% in 2025, assuming Brent at US$75/bbl. This reflects the industry’s disciplined approach to investment balanced with providing adequate returns for shareholders.

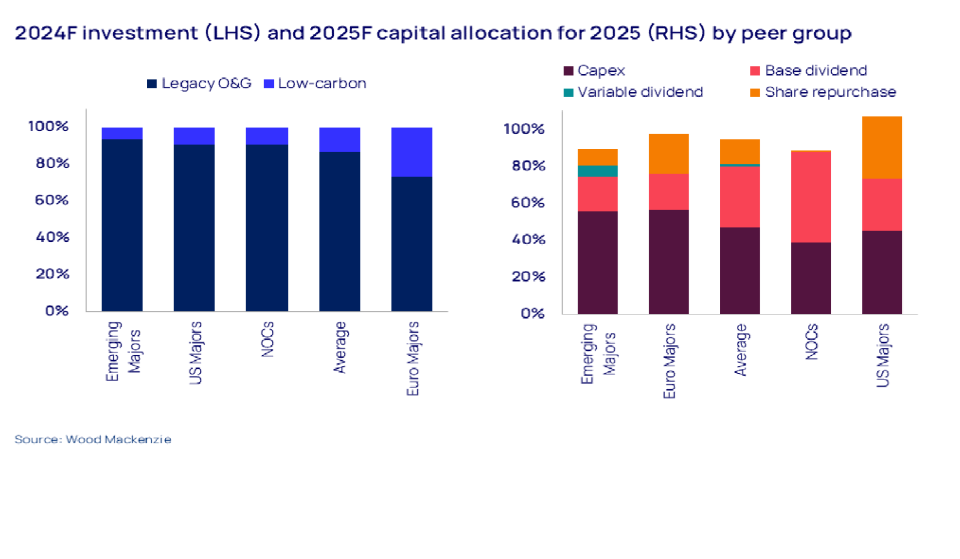

Companies are coalescing around an average re-investment rate of 50%, again assuming US$75/bbl Brent – Majors a little higher, NOCs lower. Returns to shareholders average between 35% and 60% by peer group, either in the form of dividends or buy-backs. There are outliers, of course – one or two companies with big development projects will invest up to 80% of cash flow and may require asset sales to support distributions. For IOCs, capital allocation fits within a conservative overall financial framework that includes target balance sheet gearing at or below 20% (the Majors’ average was 16% in Q2 2024, half the end-2020 peak).

Is upstream spend increasing?

Upstream still dominates across all four peer groups, in 2024 ranging from 60% of total investment for the EuroMajors to almost 90% for Emerging Majors. Organic spend in upstream is already at its highest level since 2015 in absolute terms – and we expect it to go higher still in 2025, albeit marginally.

The main driver has been the dawning realisation that the transition is unfolding more slowly than expected, implying that oil and gas demand may be stronger for longer. EuroMajors are looking to plug production and cash flow gaps by investing more in upstream. US Majors and some Emerging Majors have already used M&A to expand and extend upstream exposure. We expect more sector consolidation to come in 2025.

Exploration spend, though, is still subdued, tracking at around half the levels of a decade ago – only a few NOCs are stepping up investment. The Majors will need to consider increasing budgets for high-impact exploration as one means of replenishing portfolios for the next decade.

Is interest in low-carbon investment waning?

Far from it. From minimal levels in 2020, spend in low carbon will hit a record US$50 billion across the peer group this year. Renewable power is the big growth area. It will absorb almost half of low-carbon budgets and is expected to increase steadily from current levels through the decade.

The Euro Majors and NOCs account for almost 80% of investment in low carbon. The biggest company spenders are Shell, TotalEnergies, Saudi Aramco, BP and ADNOC. Each is investing around US$5 billion a year, more than double the next tier of companies, which includes the two US Majors. Proportionately, Repsol is the leader, committing 40%.

NOCs are emerging as the biggest spenders on low carbon. While some IOCs may soften longer term low-carbon targets, the scale of the NOCs’ cash generation and overarching country targets suggests they are less likely to dial back. ADNOC is a case in point. It’s charged with helping to deliver the UAE’s national decarbonisation strategy as well as the longer-term goal of diversifying the country’s economic dependence on oil and gas revenue.

What are the main risks to investment next year?

The implications for oil (and LNG) prices of heightened geopolitical tension in the Middle East as well as the current structural oversupply of oil. Our Corporate Strategic Planner projections for 2025 are premised on US$75/bbl Brent, which we believe is broadly aligned with companies’ planning assumptions. Any additional cash flow from higher prices is likely to be returned to shareholders or used to pay down debt. If prices are materially lower, we’d expect buybacks and/or dividends – rather than investment – to be adjusted down.

Source: Woodmac